As India’s deeptech story unfolds rapidly, venture capital players are evolving their models and thesis to this segment which has its own peculiarities and risk-to-reward mechanism. It’s hard to find a single large VC fund which is not bullish on deeptech despite known challenges such as the potentially long exit horizon, the high gestation period for maturity of products and deeptech IP.

Large VC funds may also be blind to the right networks and knowledge base needed to evaluate early deeptech startups. It’s easy to forget that deeptech is a vast umbrella sector that covers some very complex segments — everything from artificial intelligence to robotics to spacetech and of course semiconductor and electronics systems design.

Not every fund is capable of becoming a deeptech fund, so what does it take to run one?

For Bengaluru-based Yali Capital, a Category 2 AIF specialising in deeptech, that comes down to how much patience one has as an investor and whether the fund managers themselves know what it takes to build despite the complexities.

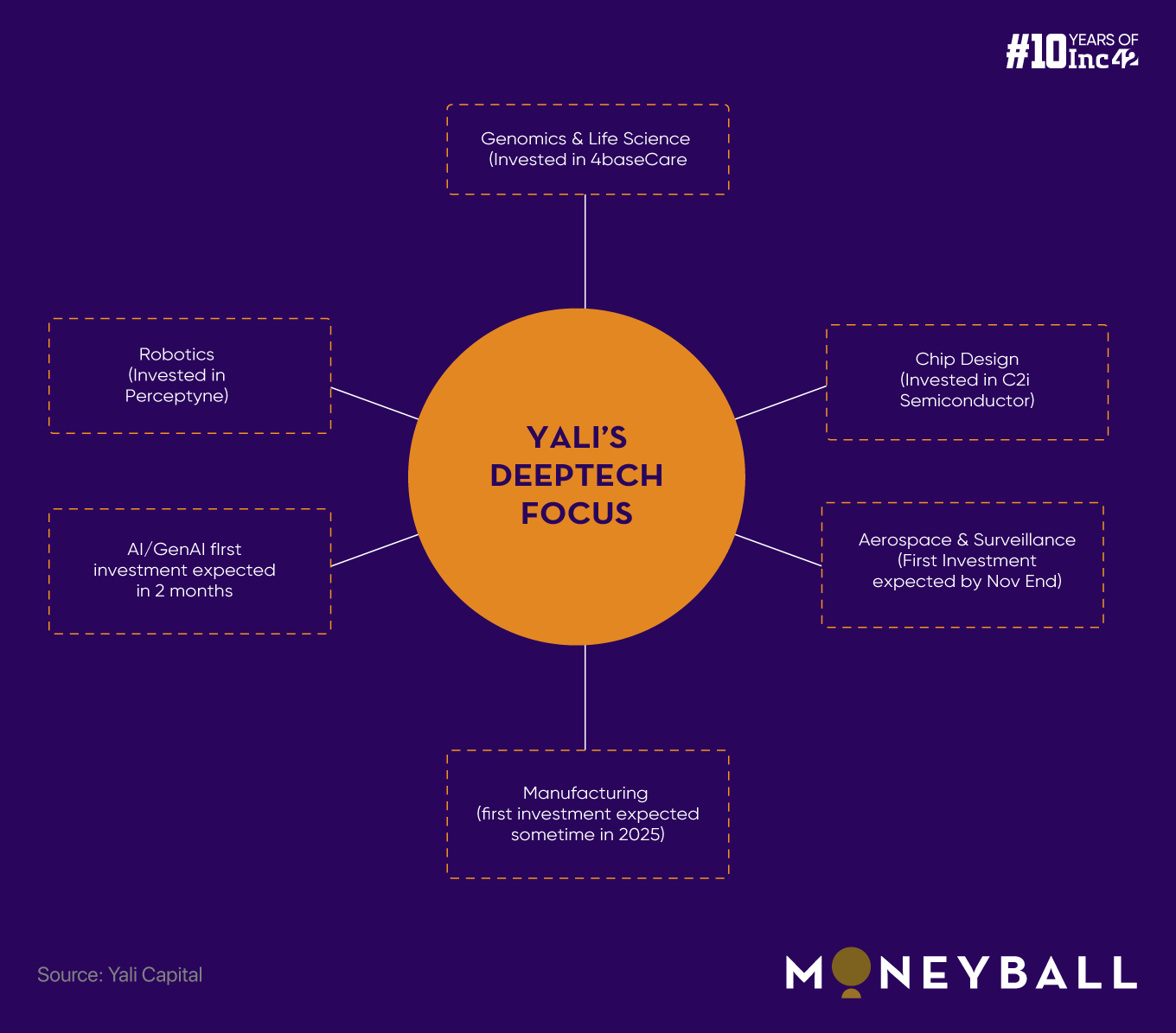

Launched in July this year with Ganapathy Subramaniam and Mathew Cyriac as founding partners, Yali Capital is a INR 810 Cr (around $100 Mn) fund looking to invest across deeptech sector and in segments such as chip design, robotics, aerospace and defence, genomics, space, manufacturing, and the wide world of AI.

Subramaniam, affectionately known as ‘Gani’ in the industry, comes with 15+ years of experience in the semiconductor space at Texas Instruments and founded Cosmic Circuits after TI. He has also personally backed listed drone maker ideaForge, and deepetch startups like Tonbo Imaging, and Aurasemi via Celesta Capital.

Meanwhile, Cyriac managed $3 Bn worth of assets as the former co-head of Blackstone India and helped companies go public in the deeptech space, including ideaForge.

The duo was joined by Lip-Bu Tan who is a globally renowned name in the semiconductor space as the former CEO of Cadence Design Systems, a board member of Intel and Schneider Electric, chairman of Walden International, and more.

Recently, Yali Capital invested in a genomics startup 4baseCare as well as robotics startup Perceptyne Robots and fabless chip design company C2i Semiconductors.

Subramaniam is bullish about India forging its own identity in the deeptech world, despite several comparisons to western giants.

Edited excerpts

Inc42: What was the inspiration behind founding Yali? Give us some insight into how you built your thesis given how vast deeptech is

Ganapathy Subramaniam: We believe that just like Silicon Valley, the Indian startup ecosystem, needs more successful entrepreneurs to become VCs. When entrepreneurs become VCs they have better ability to create larger companies as they have already walked the path.

After years of entrepreneurial journey, starting a new company would have been an easier path for me. However, the excitement now is being able to create at least 3-4 excellent companies with Yali Capital’s investments. So, with our years of deeptech experience, we are now trying to establish a strong foundation which requires capital and a connection to the ecosystem. We are trying to get the best of LPs from the US, Japan, Taiwan, and Korea.

To talk about Yali’s thesis, very clearly, we are focussed on deeptech in India. We are going to invest only in India-headquartered startups across the six major verticals. From this fund, we will put money in a maximum of 15 companies.

Of the total $100 Mn fund, nearly 25% of our money will go into chip design because we have extensive experience in this sector – I have co-founded two companies, Karthik is a chip designer, and Lip-Bu, arguably, is the best chip design investor in the world.

Similarly, we have a very strong story in aerospace and surveillance. Matthew took MTAR to the public. As a precision manufacturing company, it’s also one of the first deeptech companies to IPO in recent years. He took Data Patterns, which is a radar company, to the public. Then he helped me to take ideaForge public.

We are going to work on two more companies to go public next year. Matthew and I have a significant understanding of this space. So, another 25% will be invested in aerospace and surveillance.

From this fund, we might invest in three late-stage companies given we can exit these investments within two to three years.

Inc42: Just earlier this month Yali Capital announced an investment in C2i Semiconductor. What drove you to invest in the startup?

Ganapathy Subramaniam: We have always been keen to support entrepreneurs with a vision of creating globally competitive semiconductor design companies from India. The founders of C2i have a collective experience of over 100 years and have the necessary skill set to create innovative products in a market dominated by Western players.

Inc42: As a veteran in the semiconductor industry and now as an investor, how do foresee India’s future here? Are India-made chips around the corner?

Ganapathy Subramaniam: We continuously reiterate that while fabs are very important, equally important are the design companies. To give an analogy, while deploying buses on roads we also need to ensure there are passengers to board them. We are focussed on creating the chip design companies which will use the bus, that is the fabs, whenever these fabs are ready. Both need to progress simultaneously.

However, let’s keep in mind that today, India is not creating technology in the fab. As India progresses towards chip manufacturing, it will probably start with 20-28 nanometer chips while the world is already at 3 nanometers.

Most chip design companies here will keep getting their chips manufactured in globally renowned fabs, and as soon the Indian fabs are ready, they will migrate to the India fab. I believe that in the Initial years, the design companies in India will not bet on the fabs in the country as they might face several challenges.

So, I think only by 2027-2028, we might see some Indian fab-made chips in the market.

Inc42: Moving beyond semiconductors, how is Yali Capital looking at the aerospace and defence market? When will India have its own SpaceX?

Ganapathy Subramaniam: From drones to the payloads in drones, which include cameras and sensors, we have a big focus across this value chain. In fact, in aerospace and surveillance, we have a big focus on advanced cameras and sensors like LiDAR, thermal.

Besides, many software companies will also emerge here that will leverage AI to take all the complex and multi-sensory inputs to create meaningful analytics out of them.

And I don’t think SpaceX should be our reference. India will have its own successes, and I believe, in the next 10 years, we will have good role model companies in each of the deeptech verticals – whether it’s spacetech, chip design, or GenAI.

Meanwhile, India already has a top few companies across main spacetech verticals, such as Agnikul, Skyroot, Pixxel and GalaxEye. I am not sure if there is enough room for another few additions across the sectors like rockets and satellite imaging technology where these startups are already playing in. Will you download another food delivery app after Zomato and Swiggy? I am not sure.

So, in spacetech, India is going to be very strong for sure but we plan to invest only in the current set of companies unless a new startup comes with extremely novel technology.

Inc42: I understand that India’s deeptech story is strong given the plethora of talent and the potential for innovation, but when will we start seeing the revenue momentum?

Ganapathy Subramaniam: We already know that the revenue trajectories of the deeptech companies are very different. For example, we cannot expect a chip design company to start generating revenue at least for the first three to four years of their existence. Meanwhile, GenAI and robotics companies could probably start making revenue in the second or third years.

Some deeptech companies could take as much as six to seven years to clock revenue.

That is why we need to be patient. VCs can’t force entrepreneurs in chip design to start clocking revenue in the second year. We might not even see a big difference in the metrics of these startups between their Series A and Series B investments.

Now, I foresee two kinds of risks to an investment – technology risk and execution risk. Technology risk is we don’t know whether the technology will work. Execution risk is assuming that the technology works but if the company is able to execute it with sufficient capital without any regulatory or geopolitical problems disrupting their models.

Most deeptech investments are prone to execution risk because most of these founders already come with years of experience in building the same or similar tech.

In our opinion, if companies have technology risk, they could take at least six to seven years to make money. However, if their technology piece is dealt with, the ones facing execution risk might take less time, around two to four years to start clocking revenue.

Inc42: How likely is it then for deeptech startups to go bust? How does Yali do due diligence to mitigate risks, particularly on the execution side?

Ganapathy Subramaniam: We need to keep in mind that it’s very difficult for most deeptech companies to go bust. The deeptech companies usually have an exceptional quality team working together and important patents and IPs created, which make it almost impossible for them to get bankrupt or dissipate, as someone will come and acquire them just for the team or technology.

In fact, it is one of the advantages of doing deeptech funds, they might not grow 30x or 50x but I doubt they will lose money.

For due diligence, there are two basic and generic aspects all deeptech VCs look into – a collection of diversified talents in the founding team and a large market scope.

However, we first need to know the area of growth or the emerging scope in the next five to 10 years, because these startups will take at least four to five years to get their product out and have a brand.

Next, we need to consider the missing pieces for giants like NVIDIA, Google, AMD, Microsoft, and others. Then, we go out into the market to see which emerging companies have a reasonable chance of getting acquired by one of these giants to fill their missing blocks. It might or might not be acquired but as VCs we often have to approach the field with this mentality.

This is also why we reiterate that VCs need to have deep experience in the area to be strong in this sector. This is a key differentiating factor for funds in deeptech.

Inc42: Tell us a little about what kind of investments we will see from Yali Capital in the next few months. Will you concentrate your allocation in one particular segment?

Ganapathy Subramaniam: After the recent investment in C2i Semiconductors, which is a fabless chip design company focused on analogue and mixed-signal designs, our focus is on other segments.

The fourth company we will back is in the aerospace and surveillance space. All these investments are expected to be done by the end of November.

By December or January, we are expecting to announce one more investment in the GenAI space. In 2025, we might consider investing in a manufacturing startup as well.

[Edited By Nikhil Subramaniam]

By Inc42 Media

Source: Inc42 Media

Discover more from FundingBlogger

Subscribe to get the latest posts sent to your email.