By Latest News

The Federal Reserve’s favoured inflation yardsticks are poised to show the tamest monthly advances since late last year — a stepping stone for officials to begin lowering interest rates, possibly as soon as September.

The report, due Friday, is also projected to show 2.6 per cent annual advances in both the overall and core gauges. The expected increase in the core measure, which paints a better picture of underlying inflation, would remain the smallest since March 2021.

Since their last meeting, Fed officials have said that while they’re encouraged by the simmering down in other inflation data — including the consumer price index — they need to see months of such progress before lowering rates.

At the same time, the labour market – the other part of the Fed’s dual mandate – is still plugging along, albeit in a lower gear. A healthy job market is providing policymakers some flexibility on the timing of interest-rate cuts.

The latest inflation numbers will be accompanied by personal spending figures that will inform on services outlays after recent retail sales data showed less of an appetite for merchandise. The median forecast calls for a slight acceleration in nominal personal consumption as well as income.

What Bloomberg Economics says:

“We don’t think the slower inflation print will be enough to convince officials by the time of the July FOMC meeting that inflation is on a firm trajectory down to the Fed’s 2 per cent target.”

—Estelle Ou, Stuart Paul and Eliza Winger, economists

Among other data in the coming week are readings on June consumer confidence and reports on May contract signings for purchases of both new and previously-owned homes. In addition to the third estimate of first-quarter economic growth, the government will release figures on durable goods orders for May.

In Canada, central bank Governor Tiff Macklem is set to speak in Winnipeg, consumer price data for May are expected to show core inflation easing for a fifth month, and a gross domestic product release for April along with a flash estimate for May will also provide crucial insight.

"Chart")

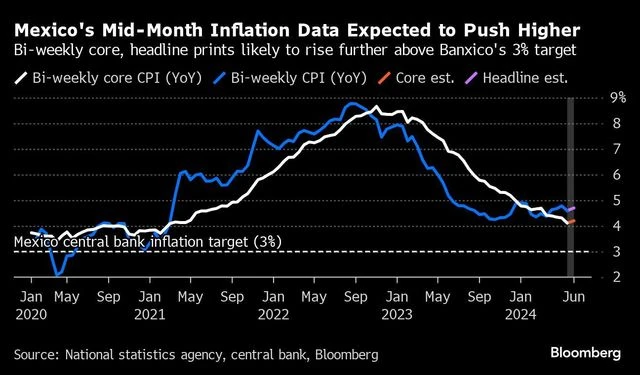

Elsewhere, inflation numbers in three major euro-zone economies may also cheer officials, while central banks in Sweden and Mexico will probably keep rates on hold.

Asia

Asia gets under way with the release of minutes from this month’s Bank of Japan policy board meeting.

The document takes on heightened interest after authorities pledged to cut bond buying, while also saying that investors will have to wait until late July before getting details about the scale of the reductions. Hints may emerge on Monday.

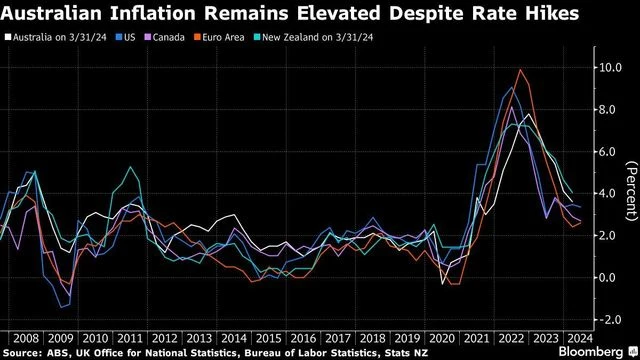

Elsewhere, Reserve Bank of Australia Assistant Governor Christopher Kent speaks on Wednesday and Deputy Governor Andrew Hauser a day later, with the focus falling on any fresh hints of hawkishness after the governor said the board considered a hike at its meeting this month.

"Chart")

Japan will see a leading indicator for national inflation trends with the release of the Tokyo CPI gauge for June. Bloomberg Economics expects inflation in the capital to have picked up to 2.1 per cent, lifted by an increase in utility prices after the government cut energy subsidies.

Other nations publishing updates on prices include Malaysia, Singapore and Uzbekistan.

In other data, China’s industrial profits on Thursday may reflect the benefits of an official push for equipment upgrades, and trade statistics are due during the week in New Zealand, Vietnam, Sri Lanka, Thailand and Hong Kong.

South Korea gets two indicators pointing to domestic demand with retail sales and consumer confidence.

Europe, Middle East, Africa

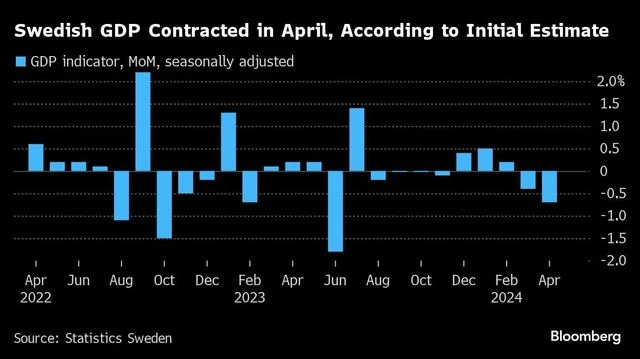

The Riksbank decision on Thursday will be a highlight, with Swedish officials widely expected by economists to pause their easing cycle after an initial rate cut last month — presaging a similar move anticipated for the European Central Bank to stay on hold in July.

"Chart")

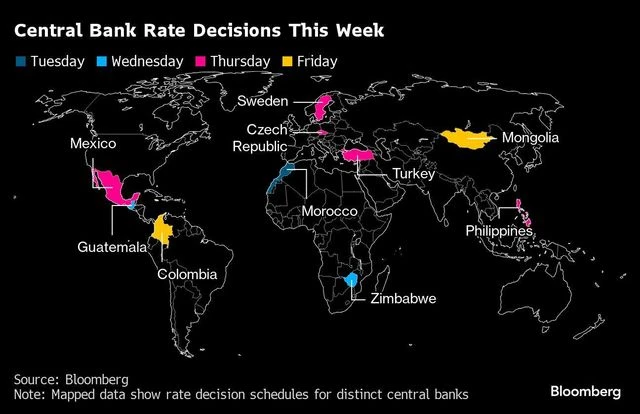

Here’s a quick look at other central bank decisions around the wider region:

-

-

-

-

On Wednesday, Zimbabwe is expected to cut its key rate for the first time since it introduced a new currency, the ZiG, in April to combat deflation. -

Czech policymakers may reduce borrowing costs by 25 or 50 basis points on Thursday, while stopping short of saying that inflation has been beaten. -

The same day, Turkey’s central bank will likely hold its rate at 50% as it waits for consumer-price growth to slow from last month’s figure of 75%. Officials are confident borrowing costs will start to drop significantly in the second half.

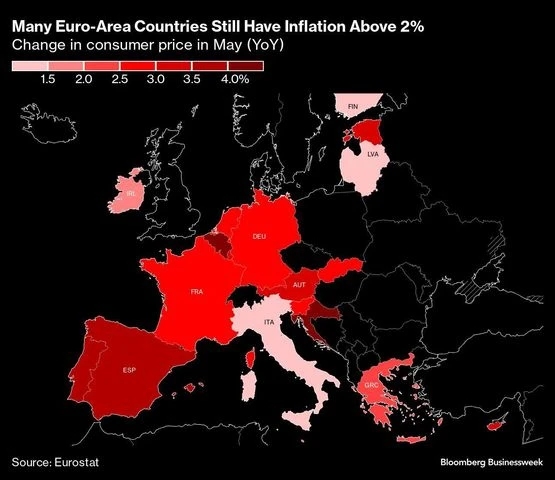

In the euro zone, inflation data in three of its four biggest economies will arrive toward the end of the week. The reports are expected to show slowing in France and Spain, with price growth staying weak in Italy.

"Chart")

Other reports include Germany’s Ifo business confidence index on Monday, which is anticipated to show further gradual improvement in sentiment among companies in the region’s biggest economy.

Policymakers scheduled to speak include Bank of France Governor Francois Villeroy de Galhau, whose economy is subject to intense investor scrutiny before upcoming legislative elections. Appearances by ECB Chief Economist Philip Lane and the German and Italian central bank heads are also on the calendar.

In the UK, meanwhile, Bank of England officials — whose June 20 decision moved closer toward a potential rate cut in August — will continue to avoid public communications ahead of the July 4 general election. Data there include the final GDP release for the first quarter on Friday, including current account numbers.

Turning to Africa, Zambia’s growth statistics for the first three months of 2024, due on Thursday, may reveal some of the impact from a devastating drought. The dry spell is expected to cut expansion to 2.5 per cent this year from 5.2 per cent in 2023.

The next day, Kenyan inflation for June will give a further indication of the impact flooding and heavy rains have had on food prices there.

Latin America

"Chart")

The central bank is the focus in Brazil as it releases minutes of its June 18-19 monetary policy meeting on Tuesday as well as its quarterly inflation report on Thursday. Sandwiched between the two is the mid-month reading of the benchmark consumer price index.

Keeping the key rate at 10.5 per cent came as no surprise, though the post-decision communique’s relatively mild tone raised a few eyebrows.

"Chart")

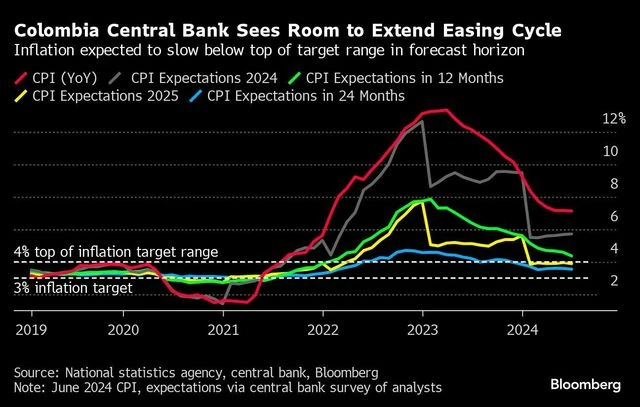

While many of the region’s other big inflation targeting central banks are either sidelined or increasingly hawkish, Colombia’s BanRep is expected to cut by a half point to 11.25 per cent — 200 basis points down from last year’s 13.25 per cent peak — and is on a path to end 2024 at 8.5 per cent.